This is the first in a series of recorded interviews for adaptive urbanism. It’s a fitting start because my guest’s work is at the foundation of the Adaptive Urbanism concept.

Michael Wilkerson works at the intersection of public policy and private real estate economics, and he is arguably the most visible economist working on Portland’s urban condition. He has authored the analyses that validate and in some cases, challenge the Adaptive Urbanism thesis.

Our conversation starts with the diagnosis. We get into the question of whether Portland’s situation is cyclical or structural, and talk about the transition that the built environment can undergo in the years to come. And finally, we talked about the response. What might we do as we step forward in the years to come?

MATTHEW CLAUDEL: You’ve presented the State of the Economy report at the Portland Metro Chamber for four years now. When you delivered this year’s presentation, and as you walked off the stage, how did it feel different compared to previous years?

MICHAEL WILKERSON: I think it felt different in the sense that we’re now building off of previous presentations with an expectation that the public is now absorbing and digesting what we have been saying.

That allows us to expand the conversation beyond just looking at leading and lagging indicators. In previous years if I said we’re in a recession, it was so novel that people needed to grapple with it. Now this is intuitively obvious. It doesn’t need 30 minutes of content around it because the data are so consistent and overwhelming. Instead of spending the bulk of the conversation there, now I can just say recession and move on without having to justify why.

CLAUDEL: I also noticed that in years past, you’ve used recovery as a benchmark, and this year you didn’t. Am I reading too much into that? Are you indicating a structural shift?

WILKERSON: That’s the point. Thinking about recovery is flawed in the sense that it implies we can go back to where we were. Even if you believed that you could do that, the time to recovery is unfathomably long. You can’t actually work towards that goal because it’s a decade or more away.

Rather than trying to say, can we get back to where we were? I’d like to see theories emerging around what the future might be, assuming that it is going to be different than the past. We don’t know exactly what it’s going to be, but we cannot assume that we’re going back to where we were and that the playbook is known and that we can redeploy known policies that have worked in a previous structure. In the last year, that clarity emerged. Now it’s near irrefutable.

CLAUDEL: What gave you that sense of clarity?

WILKERSON: We saw certain indicators showing what seems to be a recovery, but those reversed in a way that suggests it wasn’t actually happening. There hasn’t been a reversion to the mean—it was noise. We always get the question are we at the bottom? Are things about to get better? But there is no bottom. The idea of a bottom indicates that we are going back to where we were.

CLAUDEL: If I understand what you’re saying correctly, it’s that we need to actually have a structural shift in how we think about the supply that meets a new form of demand.

WILKERSON: That’s right. We need to be talking about demand because the nature of demand has changed. Instead of prioritizing how do we align the supply with the demand, we need to focus on what is the demand now, and what is it going to be? It’s a demand issue primarily, or certainly a demand issue that needs to be looked at in combination with supply. It’s not a market failure solving for some cyclical nature, that just needs a temporary fix because the structure is still aligned in the future.

CLAUDEL: I want to come back to this and the difference between a cycle and a cliff and how we might actually put numbers behind that difference. But first I want to call out one of the most dramatic numbers in the report. One that you and I have both used in presentations. It’s very effective.

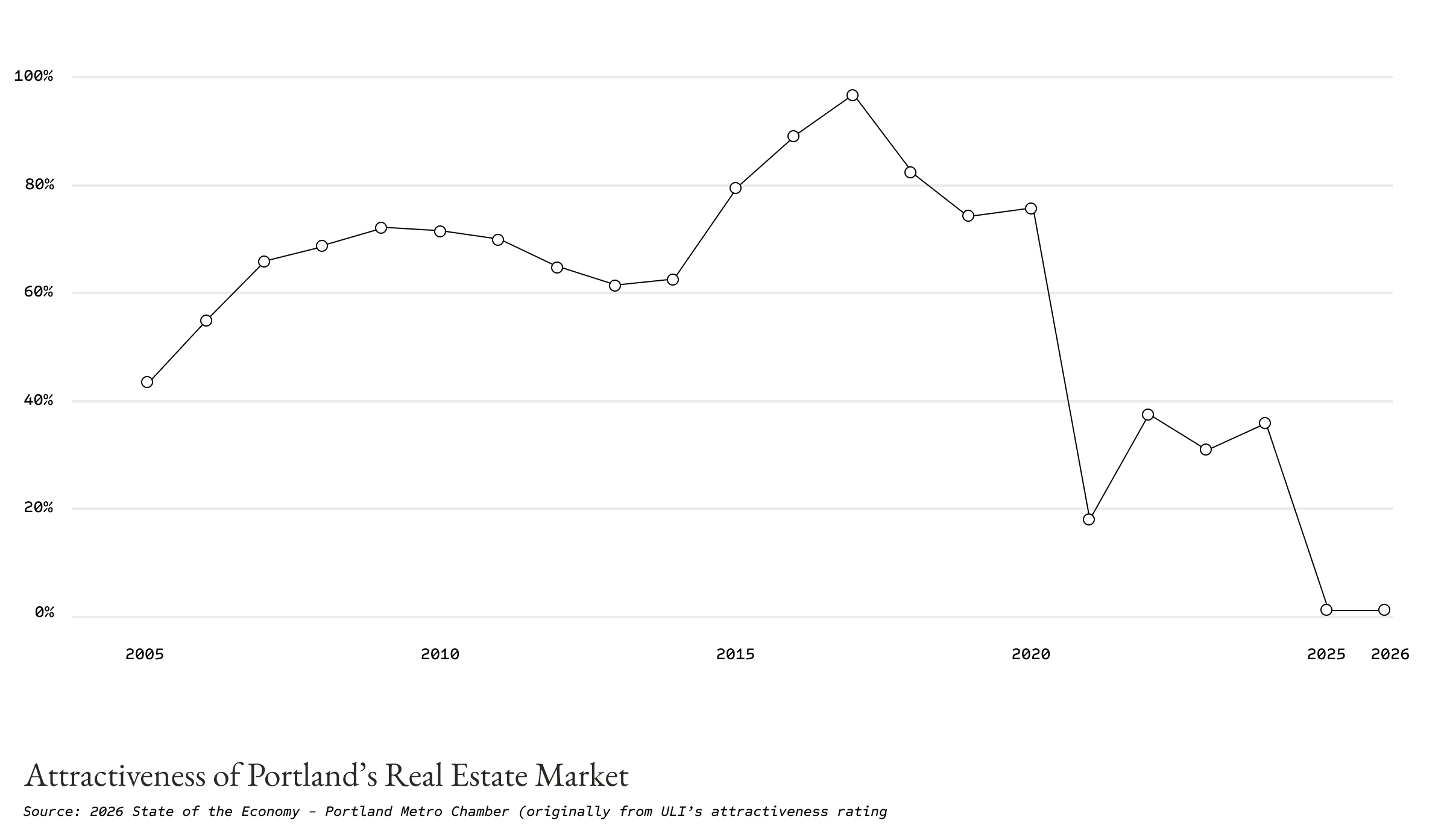

Portland is 80 out of 81 in ULI’s development attractiveness ranking. Not seven years ago it was near the top. We’ve had a precipitous fall in development attractiveness. But in a sense it’s an indicator of the creativity of the development market because development attractiveness is related to factors like rent growth expectation and cap rate compression potential, population growth, job growth – the traditional indicators.

In a world where the previous market fundamentals held, Portland is an abject failure, but if those aren’t the relevant fundamentals going forward, maybe there is a disconnect in a market opportunity. Of course Portland is not going to compete in the old game. But can we compete in a new one?

WILKERSON: That’s the realization that we’re having now. If we thought we were going to be one of the top 10 fastest growing metros from a population and jobs standpoint… no, we are not. Certainly not in the near term. From that perspective, yes, the ULI ranking is actually valid. But is it measuring the wrong things?

CLAUDEL: Exactly. That’s the question.

WILKERSON: Historically, it has been a leading indicator. When the structure is not changing, the ULI ranking is actually a very good leading indicator because it measures sentiment and sentiment reflects future development decisions.

Developers in the aggregate are not risk takers. On an individualized basis they very much are, but they’re not going to move together into a place of risk. There’s going to be a person who moves into a market individually and that person typically gets outsized returns and eventually that becomes the market norm. That’s where we are in Portland. We need to have one or two catalytic projects, and then the process starts. And at that point, we will jump massively in the rankings.

There is no silver bullet. There isn’t even a list of 10 things that you could do today in Portland to demonstrate that this is a new norm and that Portland is adapting. I used the analogy of Groundhog Day. Until the catalytic project, there is nothing that is going to change that perception of Portland through the lens of the old structure. We deserve our ranking.

CLAUDEL: Right, because the ranking measures essentially the bulk of the bandwagon. Portland does have a massive inventory of distressed assets. There is a huge untapped potential for upside from repositioning buildings. So it could be that we’re scoring poorly on conventional metrics, but we have opportunity in terms of alternative investment strategies.

The question is: how much contrarian capital is out there? What you’re saying is that we need a couple lighthouse projects. Those will only happen through contrarian capital; an alternative investment thesis. Those lighthouse projects will cause the bandwagon to change its direction, and then we will see a jump in the rankings. We need to re-rack the market.

WILKERSON: Yes, and I think one of the ways it gets re-racked is vacancy rates and capitalization rates for any given building.

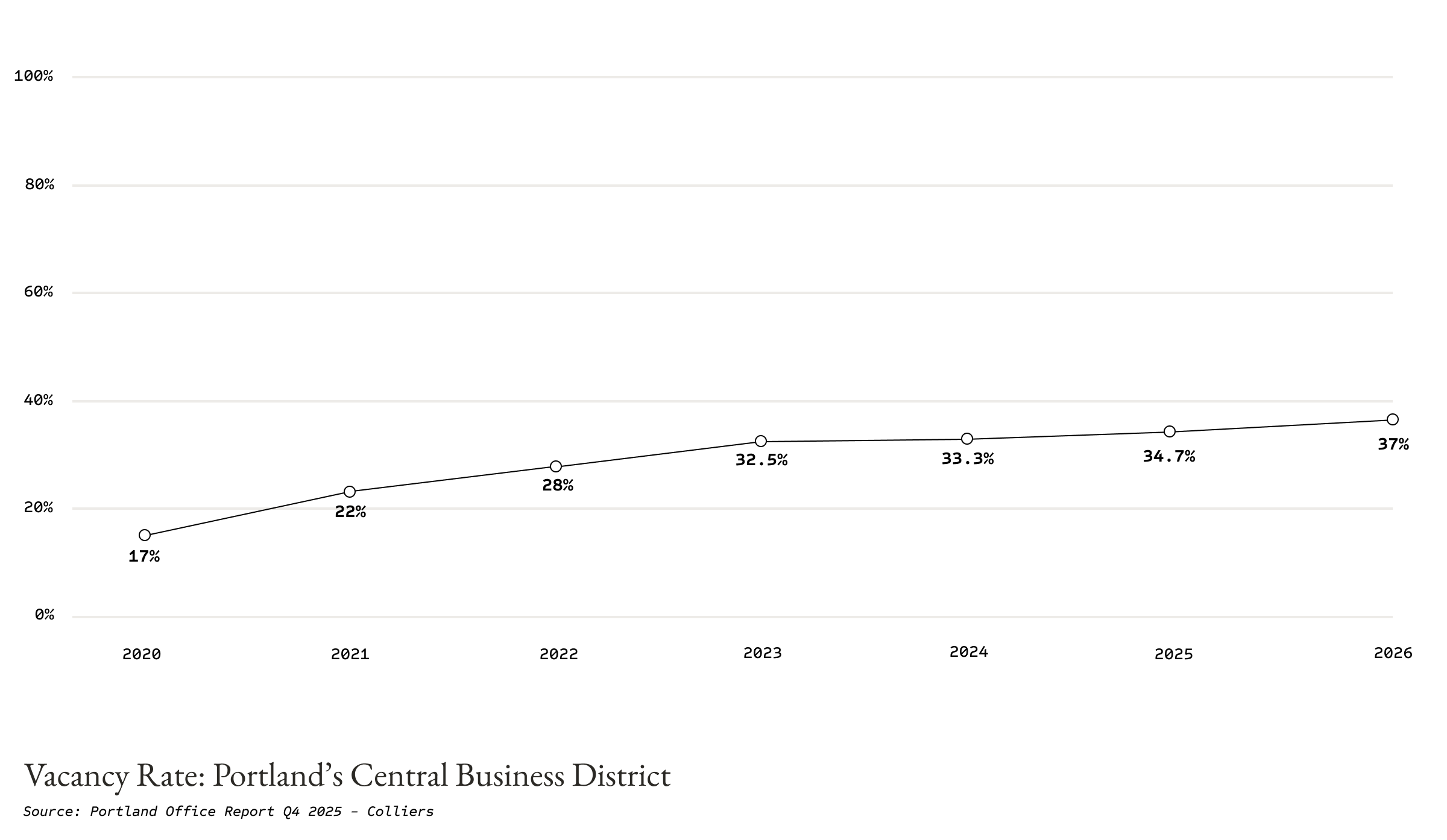

CLAUDEL: Broadly this report projects that vacancy is going to peak and then gradually decline. But we’ve also argued that there is a structural threshold, at 30% or 40% vacancy, we will see an accelerating decline. You and I have also talked about the reality that leases written before the pandemic are going to be expiring in the next year or the one after. The reason that’s important, beyond the vacancy rate itself, is that a lot of debt that was structured pre pandemic, in a very different interest rate environment, is now going to be maturing into a very high interest rate environment, and that’s happening right as the vacancy cascade hits buildings. It’s a recipe for foreclosure.

Help me understand where you see this going. Are we going to hit a bottom on vacancy then stabilize, or do you think this is a cascade has yet to emerge in its fullest expression?

WILKERSON: I think what you’re suggesting is very plausible. A year ago I would have said it was plausible that we were going to hit a peak and have a stagnation to very slow recovery.

Now, if you look at the leasing volume in this last year in the central city, it’s around half of what it was one year ago, and it’s lower than it was in 2020. The data suggests a real possibility that we are not seeing a peak vacancy rate, and that we may not hit an actual peak ever. Or if we do hit a peak, that it won’t inevitably be followed by a recovery.

There was a period of time when Portland was a tech satellite. That recruitment strategy, paired with domestic natural growth, got us to that point where we were the darling of the ULI rankings.

Why would a company choose to locate here today? The answer is they aren’t. We are no longer a tech satellite. The data could not be more clear: it’s one way traffic. There are no large leases of any kind coming into the city. More problematically, the companies who are here aren’t growing organically or investing to grow.

Understanding that we cannot rely on that specific kind of recruitment is going to be very challenging, and we just don’t see examples of organic growth happening in this market because the comparative nature of operating a business here is such that you can’t extract a competitive advantage.

CLAUDEL: What you’re implying is that in the past we also had an X factor, which was the quality of life and the agglomeration effects of the streetscape. We had a comparative advantage. That is why tech companies put satellite hubs here, because people wanted to be here.

WILKERSON: Companies could operate more profitably, having remote workers at a time when remote wasn’t a thing. Now that remote is a thing everywhere, you would think we should be absolutely dominating, but it’s the opposite because we have eroded our comparative advantage.

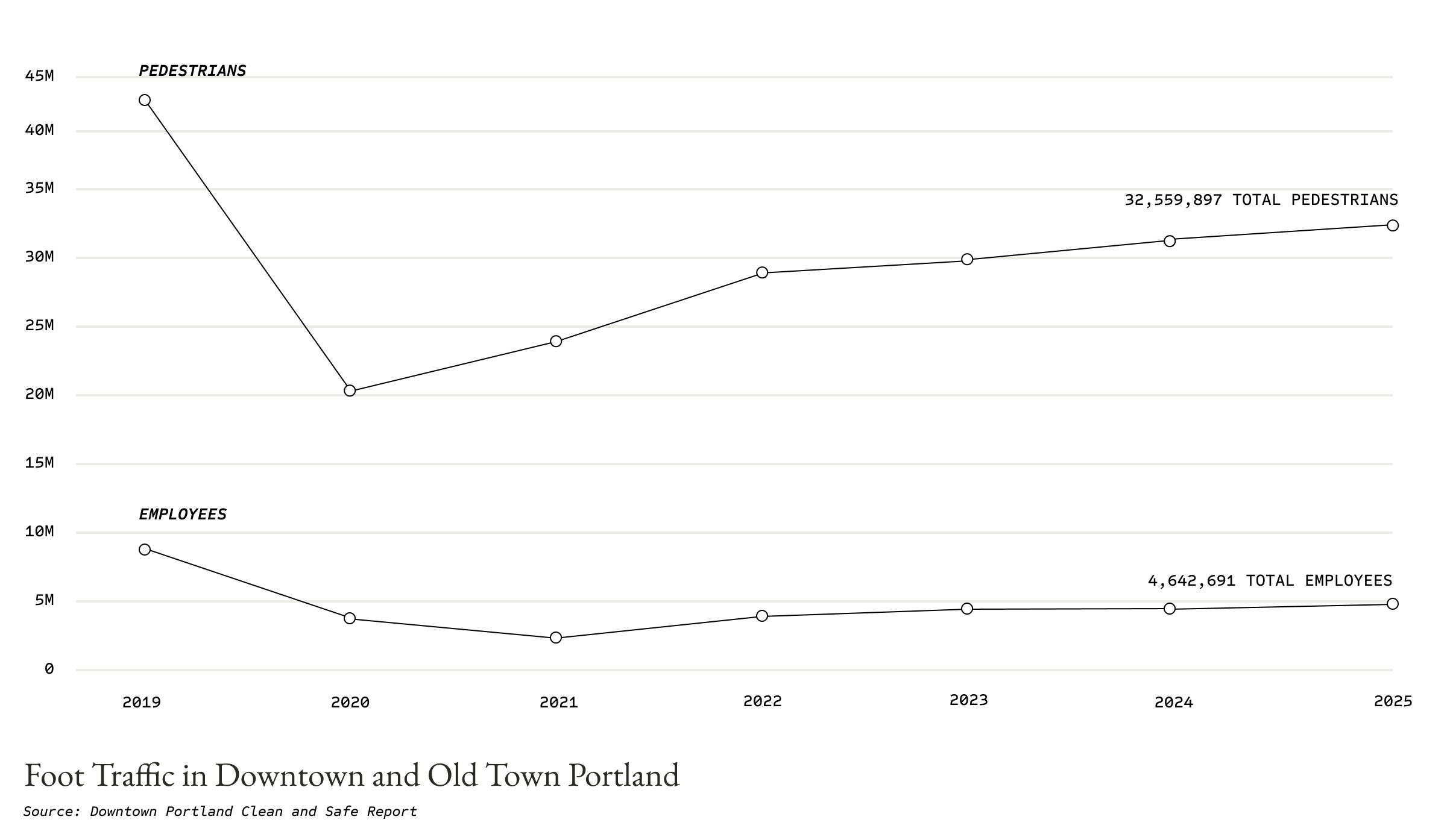

CLAUDEL: Competitive and comparative advantage points back to something interesting I noticed in the 2026 State of the Economy report. There is mathematic barrier to trading on our X factor. You found that even a full return to office would only get us about halfway to pre-pandemic downtown foot traffic. This was shocking to me.

You’re essentially making the case that the old single use downtown model can’t work.

WILKERSON: Correct. Even if we get back to full occupancy, the old model of downtown cannot work. This is what we have been saying. This is not where we should be spending our energy. It’s not that full occupancy wouldn’t help, and some businesses might even opt into it as an individual business decision.

If the hope is that full occupancy is the strategy that’s going to “get us to recovery,” it’s a mathematical impossibility. We should understand that reality for what it is, and then talk about alternative productive strategies.

CLAUDEL: So what is downtown? What do we want it to be?

WILKERSON: Yes, we have to think about what downtown’s value proposition is in the context of our broader central city. The problem for downtown is that we have what I would describe as a new mixed use character in many of our other central city neighborhoods.

When you look at the streetscape, at the block level, our concentration of problem areas is immense, while there are pockets of strength around them.

What are the big targeted interventions that can provide enough of an anchor that you could transform downtown in a strategic way? A lot of people are saying it just needs to be more housing. But is there a plausible value proposition for a resident to move in as the first tenant of a transforming downtown?

Maybe, but if it has to be massively subsidized, we need to be clear about the implications. And maybe the answer is that there is no value proposition. If that’s the case, then Portland’s downtown needs to transform itself into a different type of thing, contextualized by the rest of the central city.

CLAUDEL: So if I could simplify what you’re saying into a dichotomy, the neighborhoods around the central city are, in a sense, becoming more like historic downtowns, because they are now places where people work. What if downtown becomes more like a historic neighborhood? That hypothesis is why we’re now having a conversation about office to housing conversion.

Now, I think it’s worth looking back at the housing conversion study that you worked on. You found that, and correct me if I’m wrong, only about 5% of the building stock is amenable to housing conversion. There are a lot of headwinds, right? We have architectural headwinds. We have policy and land use and building code headwinds. Cost is obviously a headwind.

Conversion is just very challenging. You just brought up an interesting one, which is the cultural headwind. Here we are, sitting next to Nordstrom, right off of Pioneer Square. This works as a business district, but it doesn’t really feel like the kind of place where I want to have my kids running around.

WILKERSON: It’s not an after five o’clock neighborhood.

CLAUDEL: It is not an after five o’clock neighborhood. I’d call this a cultural headwind. So I’m curious, how should we think about office to residential conversion? Are we seeing that the decline in the actual acquisition cost of any given piece of real estate now is making the financial piece maybe more viable? Does that change the balance of headwinds and tail winds?

WILKERSON: No, unfortunately. In that report we were projecting into the future, to a time when acquisitions could happen at $50 a square foot. They were not happening at that point then, but they are now. That is to say, we were already looking ahead to a future state of distressed acquisition. So no, there is no possibility that the value of the buildings could drop so much so that it would alleviate the need for other interventions.

For office to housing conversion to be viable, you still need other interventions. That was the “aha” moment in the conversion report. There is a need for structural changes to fire and life safety codes. Until you do that, nothing else matters. On top of code amendments, there are a handful of necessary but insufficient conditions, like SDC waivers, tax exemptions, and per-unit subsidies.

The question is, structurally, can that even happen today, or is it just a market impossibility? I’m not saying definitively yes or no. I’m saying we need to explore that “if” statement. If this is an impossibility, then trying to build units of housing will be a failed policy.

I’ll use SDC waivers as an example. Three years ago, SDC waivers would have been immensely valuable. We weren’t ranked 80th out of 81. At that time, the market was close enough to delivering housing, and SDC waivers would have been a signal.

The thought was that SDC waivers would generate thousands of units. Now we can see that it has done effectively zero. So there are still tons of headwinds. You’re not going to see the market respond to the opportunity for conversion without just moving mountains.

CLAUDEL: We are pushing an immense boulder up a hill.

WILKERSON: Exactly. The intention is not wrong, and 2,500 units of housing might be the ultimate outcome.

The bigger question is really around sequence and timing. If this isn’t a neighborhood, a place for families, what do we need to do to make it so? Do we need to build parks? Do we need to build a children’s museum? Do we need to build more arts and entertainment and cultural things?

Maybe the long-term strategy is changing the value proposition of downtown versus trying to subsidize office to residential conversion in an unscalable way. It might not be an optimal strategy now, at scale. But if the intention is to make downtown a neighborhood, there need to be many targeted interventions between now and then, and maybe it can happen. I would rather not wait for five years to then realize, oh, we weren’t ready to do that yet.

CLAUDEL: What if we take a step sideways? Residential is not the only target for conversion. Suddenly you’ve eliminated a lot of those headwinds, specifically the structural and fire and life safety issues, which bring huge costs, and obviously the associated zoning questions. I wonder if there might be a near term strategy for putting some of this square footage to work before we see the fundamentals of residential start looking different.

WILKERSON: That’s the hypothesis that makes more sense in this moment. And you’ve done a good job of starting to outline why that is the case.

CLAUDEL: What sorts of targets could you imagine? What do you think would be the most interesting?

WILKERSON: I think this is part of the challenge for Portland. Today we’re hearing we need an economic development strategy. We’ve evolved the conversation, but when seven different economic development strategies are happening at the same time, they’re very unlikely to be aligned.

We’re trying to eek out some competitive advantage – what will allow us to do that? The answer, to me, is that we probably need to do the thing that is politically challenging, which is to say we don’t know, and we’re going to take a varied approach, some of which will work and some of which will fail. And here is our plan to mitigate the impact of failures.

Trying a one-off only approach and thinking that you are going to succeed – that is unlikely to happen.

CLAUDEL: One of the most important, if not the most important role of an economic development strategy is to say what we are not going to do.

WILKERSON: Correct. I would argue it’s the only thing you’re really trying to do with an economic development strategy. It’s hard to know what you are going to do. But if we can be clear about what we are not doing, that is way more helpful. People can react to execute around that.

CLAUDEL: Exactly. You need to say, these are the outcomes that we’re working toward, and then we’re going to allow for the creativity and the exuberance of the market, with specific regulations and incentives built in.

WILKERSON: Build the sandbox for us and then we’ll figure it out. Don’t build the sandbox so small and prescriptively that it won’t work well.

CLAUDEL: And also make sure that there aren’t seven different sandboxes. There is a huge risk right now in Portland and in Oregon more broadly that everyone comes up with their own economic development strategy.

WILKERSON: Finally we all agree that we need something like this to progress, but maybe we need to pause a little bit.

CLAUDEL: You’ve said before that these reports are data for the conversation, not a list of solutions. But if we could take a moment, Mike, I’d like to hear your own speculations about what we might need to move forward today, especially as you’ve presented this report now four or five years running. How has your sense of what we need to be doing sharpened and what are the near term and longer term levers that we should be paying attention to?

WILKERSON: I get asked this question all the time. What would you do? And my answer is we have to understand what we’re optimizing around first, before we can talk about what we would do.

What is clear is that we have a demand problem. That is foundational to everything. And our historic policy interventions are ill-equipped or not equipped at all to deal with that. That’s a challenge.

Our tax structure is so flawed and limited that it severely impacts demand. If our tax structure in Oregon is taken as a given and a status quo, we can have a conversation about what actions we should take.

Alternatively, rather than trying to come up with an ill-equipped solution within the status quo, to me, a logical first step is structural reform. At that point, we could do very different things that would be much more likely to succeed. The challenge is that structural reform is, at minimum, a three year process.

Your question is what would I do? My answer is we should work towards that three year process. That’s a tough political decision, to say there’s a pathway here, and we are willing to take the time and energy to do the hard thing. In the meantime, are we going to implement a solution that we know is entirely insufficient because it’s better than doing nothing?

CLAUDEL: You’re very genuinely asking what the parameters of our action are. You also implied that there’s an issue of knowing, based on data, when the right action needs to be taken. You’re a data guy…

WILKERSON: I look at data occasionally. It’s true. Or you can say I live in it, a little bit.

CLAUDEL: We’ve been advocating for the idea that cities need to shift from a prediction paradigm to a learning paradigm, because no matter how much data we have, we can’t predict what the next five years, let alone ten are going to look like. I’m thinking this also relates to a comment you made a minute ago about creating the sandbox and then allowing ourselves to play toward the optimal outcome.

WILKERSON: Optionality is critical in this moment we are in. You and I both agree with that. But that is very different from the traditional paradigm in commercial real estate, and it is not what people traditionally want to hear.

CLAUDEL: Optionality has a cost. Why would we do that? Why would we build in optionality? Well, if you consider real options modeling or expected utility or risk adjusted returns, this is very clearly the right path today.

You can price risk and you can think carefully about what sorts of actions you should take at any given threshold once you see it. But you shouldn’t try to predict exactly when you’re going to see it, or which threshold you will reach. So let’s advocate for better data, but let’s also equip ourselves to be learning as best we can, as we’re taking action. So, with what data should we be furnishing ourselves as we step into this uncertain future?

WILKERSON: That’s a great question. We have to understand the totality of whatever we’re trying to capture. So if that’s people, jobs, income, GDP, what is the entirety of that? And then we can look at what our share of that is, what our trend in that is. Maybe, for the purposes of comparison, we can look at what others are doing, so we can understand if we are actually treading water? Because we have to abstract it up to a big enough observable thing that we can actually understand it.

And then I think we’re seeing emerging indicators that are more real time that we can start to get at. Foot traffic as an example of this, and pairing consumer spending with foot traffic with other things starts to give us a more real time understanding of what’s happening. There is a whole slew of proxies that we can start to build to get at some more cultural questions.

CLAUDEL: I was here on Saturday at Pioneer Square to see the winter lights, and it was packed. People were loving the winter lights.

WILKERSON: Absolutely. That’s a huge example of a successful targeted intervention that’s clearly delivering benefit.

CLAUDEL: So having a more attuned understanding of where culture is moving as people think about the value of downtown and the reasons for coming down here. We need data to understand what overcomes the magnetic pull of Netflix and the safety of a neighborhood. We need to understand what the cultural drivers are at any given moment.

So final question. You’re an economist. You teach at PSU in the real estate program. You live in Portland. How are you going to approach the State of the Economy report differently next year? And what are you going to be keeping your eyes open for, over the next year as you work toward writing that report?

WILKERSON: It’s an interesting report because I think for some people it’s a once a year opportunity to get a checkup of what’s going on.

In my mind, we’re doing a state of the economy report on a monthly basis. It’s the sum of all the work that we’re doing through a variety of clients. It always evolves, and as we get into the Fall we already generally have a sense of what’s going on.

In this particular instance, we have so many ongoing or soon to commence economic development efforts, strategies, et cetera, that are gonna play out largely through the Fall. I think that will be very indicative of what the need is at that moment in time. Are we going to say we were unexpectedly very coordinated here, and this actually is now something that we can begin to prioritize and execute on? Or will we have the seven different sandboxes problem? And is seven sandboxes better than zero? Probably. But we need to get more coordinated around it.

With near certainty I can say that the lagging indicators are going to be exactly the same. Nothing we’re doing now (and this is the hard conversation) is about changing the next 12 months, in a meaningful way. Hopefully we can sit down and have this conversation again in a year and we’ll see how prescient we were with our thoughts.