This is the seventh in our Adaptive Urbanism series. Each week, we go deeper into the challenges and the responses. Last time, we examined the institutional imperative — why adaptive urbanism requires a new kind of steward, and how the interests of public, societal, and private capital might be bound together by design. Today: why the capital markets that should be funding the adaptation of our cities are instead walking away from it.

Although the majority of meetings are now video calls, we have all had in-person meetings over the past two years. For me, one stands out, in particular. I parked in the building, walked into a vaulted lobby with a manicured green wall, and I was met with a crisp greeting from uniformed staff. I craned my neck to see the well-appointed fitness center before shooting up to the right floor. The floor was bustling with tenants. We used a conference room that was perfectly provisioned with technology that worked effortlessly. My host showed me the private, landscaped roof terrace on my way out, where tenant-only yoga was about to start.

Another meeting stands out, too. I circled the building a few times before parking several blocks away. There was a for-lease sign on the ground floor retail space, and the lobby was dingy, dusty, and desolate (the primary decor was a bright yellow “wet floor” A-frame sign). The elevator crept up to a floor where lights flickered over dated carpet, drop ceiling tiles crumbled, and my host – the only lessee on the floor – had to apologize for the stuffy air. “Something’s wrong with the HVAC.”

These two meetings happened in the same city, maybe even on the same block. Same urban fabric, same planning authority, but worlds apart.

The first building is filled with creditworthy tenants on long leases, and the landlord is backed by institutional capital. The second building is a perfectly good structure, well-located relative to transit, but facing vacancy and decline. This is a national trend, and the data is clear, but it takes boarded windows to make the reality visceral: while Class A offices absorbed 5.2 million square feet of new tenancy across the United States in 2025, the rest of the market lost occupied space in the same twelve months.1 The buildings filling up and the buildings emptying out are often on the same block.

This is not a market failure in the conventional sense. The capital markets are functioning exactly as designed. The problem is that they were designed for a world that no longer exists.

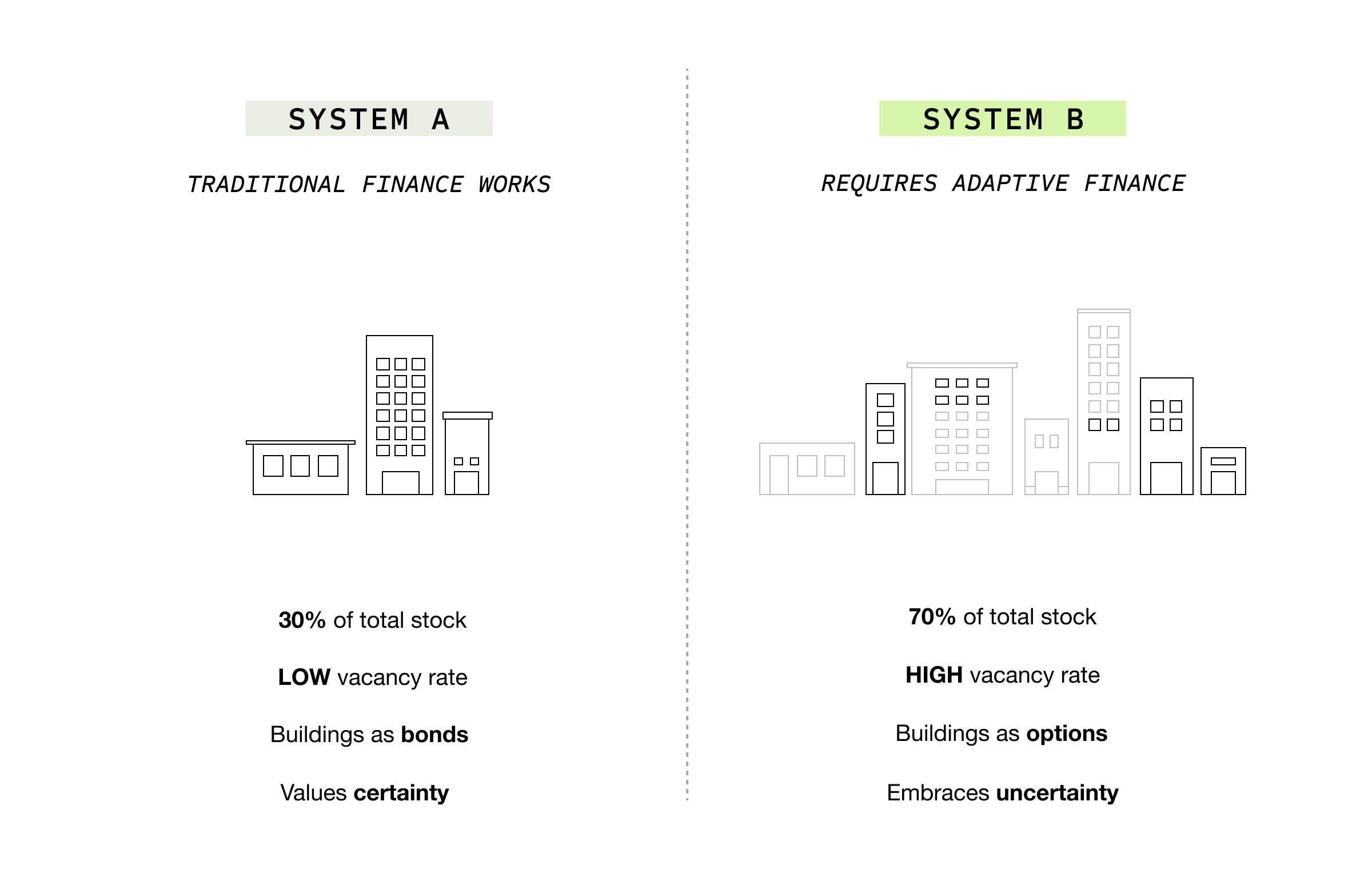

The commercial real estate market has quietly split into two domains. The distinction between them is the most important thing happening in real estate finance, and almost no one is talking about it clearly.

System A comprises the specialist assets where traditional finance continues to work: high-quality amenity-rich offices, data centers on twenty-year hyperscaler contracts, life sciences campuses, logistics facilities at critical supply chain nodes, prime towers leased to anchor tenants for whom the address is a business signal. Demand is definable, tenants are creditworthy, and leases are long. Discounted cash flow works well.

System B is everything else, comprising approximately 70% of commercial stock. Class B and C offices, aging retail, downtown mixed use, mid-rise buildings in outer neighborhoods, suburban strip malls. These buildings are not obsolete enough to demolish and not specialist enough for System A capital.

The crisis is in System B. These buildings could adapt, but adaptation is rare – it takes capital and creativity, and an appetite for risk, in situations where traditional investment models don’t work.

The numbers are stark. In the United States alone, more than 217 million square feet of office leases are scheduled to expire in 2024 and 2025, and over 800 million by 2028: the largest wave of tenant decisions in commercial real estate history (CRED IQ). Portland’s downtown office vacancy rate of 34% is among the highest of any major US city. Much of that space will not be re-leased on existing terms. Whether these buildings adapt or atrophy – and ultimately, whether Portland’s downtown survives or withers – is primarily a question of how investors model the return on capital.

Many System B buildings have adaptation potential; comfortable floor plates, tall ceilings, regular column grids, overbuilt structural engineering. The Five Oak building near Big Pink (a building we’ve looked at before) is a good example. The building could become an upgraded office, residential, ground floor retail, early childcare, self-storage, advanced manufacturing, or a mix of several uses, depending on decisions nobody has yet made.

Adapted System B assets can be profitable as these uses fulfill local needs. In a normal stable market capital flows toward profit – but that isn’t happening. Why? It’s a measurement problem. The instruments designed to value and finance these assets were built for System A, and applying them to System B produces not merely imprecise answers but systematically wrong ones.

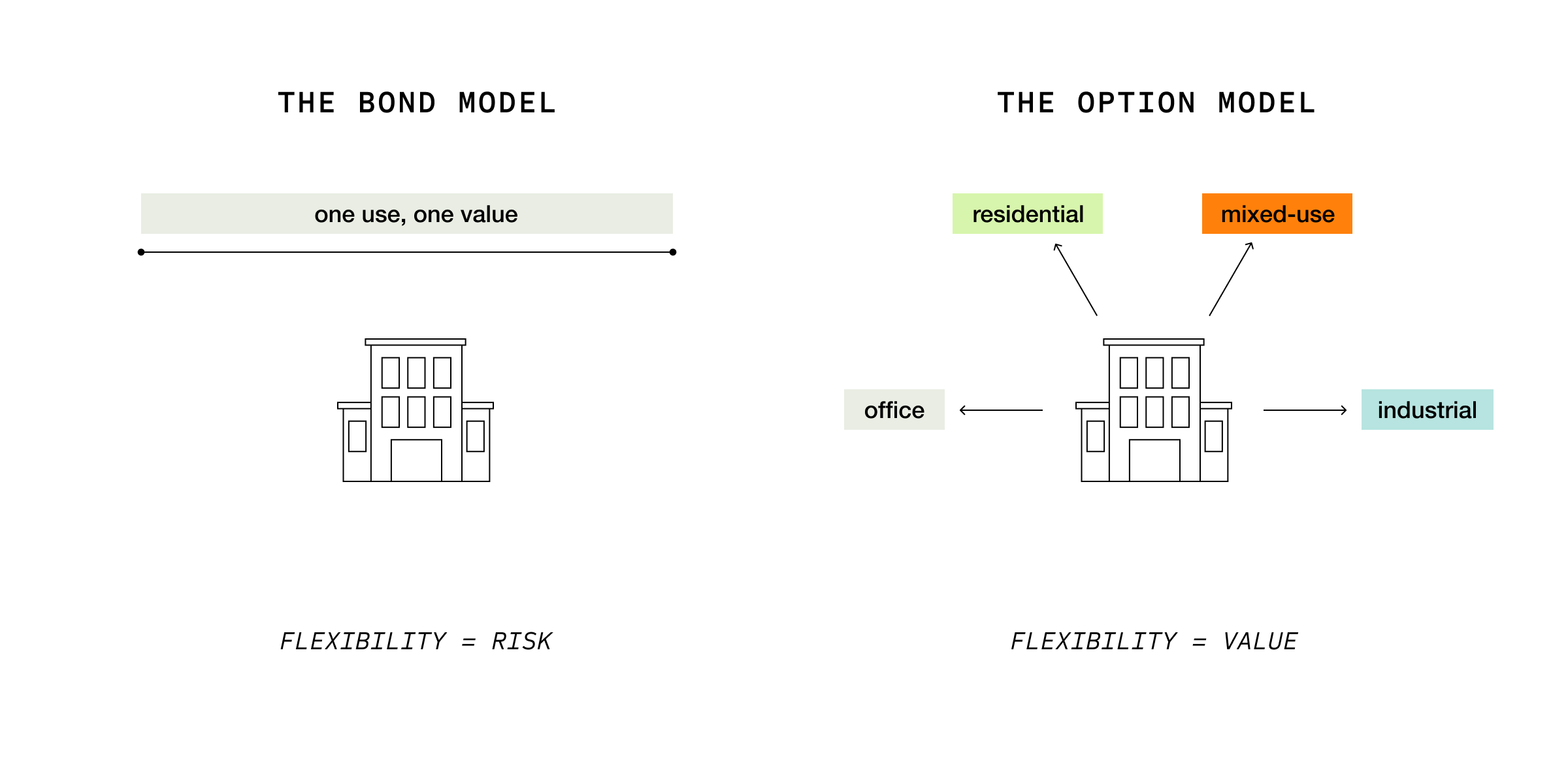

A standard discounted cash flow (DCF) model assumes you can project rental income with confidence, calculate a terminal value based on a use that persists, and apply a discount rate that reflects quantifiable risk.

All three standard DCF assumptions break simultaneously. The analyst cannot agree on stabilized occupancy, lease-up period, or $/sf lease rates. The terminal value becomes speculative at best. The discount rate is chosen to produce a comfortable number rather than something derived from analyzable risk. The Swickard Group bought the building at a steep discount, based on intuition, grit, and a strong belief in Portland – not financial projections.

“Every great city goes through its hard seasons,” Swickard said. “We just have to decide if we want to lean in or not… In the case of what we’re doing, we’re leaning in and we’re not trying to time the market. We just have a long-term belief in Portland and the people of Portland and Portland’s identity,” (quoted in KOIN).

DCF, applied to adaptive assets, systematically undervalues them. A building capable of pivoting between uses appears, through the DCF lens, as a building with uncertain income; a risky building deserving a lower value. Its flexibility – a strategic advantage that makes it valuable – is coded as uncertainty that makes the building dangerous. From a traditional investor’s perspective, dangerous buildings don’t deserve additional capital; they should be held indefinitely, or sold. The result is that adaptation never happens.

To paraphrase Antony Slumbers: we are valuing buildings as bonds in a world where they are options. The bond model assumes a fixed income stream, known in advance. The options model applies methods used in financial services to assess the prospective future value, at a fixed point in time, of an asset under different conditions. The owner may have multiple options at multiple junctures; each will have a different cost and future value. Under genuine uncertainty, option value is not marginal. It is a building’s strategic advantage.

This inversion matters enormously. If uncertainty increases the value of adaptive capacity – and it does, by the same logic that makes financial options more valuable when volatility rises – then conventional valuation methodology points in entirely the wrong direction.

The mispricing creates an opportunity.

Some investors understand System B as a distinct asset class: not a failed version of System A but a different game with different rules. They see the value in buildings acquired at significant discounts to replacement cost, in locations with genuine underlying demand, capable of serving uses that System A frameworks cannot. They have the capital and creativity needed to play the optionality in a strategic way.

Jeff Swickard is not alone – we are seeing this strategy starting to emerge in Portland. Buildings are transacting for pennies on the dollar: The Merchant Bank Building (80% of prior sale), Downtown Portland Marriott (63% of prior sale), Gus J. Solomon U.S. Courthouse (sold for $1.8 million), and of course Big Pink (12% of prior sale).

The arbitrage potential is extraordinary. Returns are imminently achievable, as Portland’s downtown rebounds – and that will depend on these buildings coming to life, and a generation of others following suit.

The instruments for that transformation are missing, however. Four things need to change simultaneously.

Valuation must evolve. Real options theory offers the alternative to standard DCF models: they assess a building’s total value as the intrinsic value of its current use plus the option value of its potential futures. That option value is calculable – it is given by the range of plausible uses, the conversion cost for each, and the returns for each, with a volatility factor based on timing and depth of demand for each. Buildings with low conversion friction and broad demand diversity carry substantial option value that conventional appraisal simply cannot see. Unfortunately, this methodology is not mainstream amongst CRE professionals (Field States is solving that problem with a light software package that runs a heavy math engine for DCF + Real Options Modeling – to be formally announced soon).

Debt must accommodate transition. A standard commercial mortgage assumes the building will serve the same purpose for ten, fifteen, or twenty-five years. For System B assets, that assumption is the problem. Covenants built around debt-service coverage ratios calibrated to a single use trip into technical default precisely when an asset is doing what adaptive finance should enable: moving between uses. Adaptive debt structures accept that metrics fluctuate during transitions and treat planned adaptation as a strategic moment of operational transition, not distress. Again, these products are not mainstream, but Field States is helping to define adaptive capital stacks that blend the most appropriate instruments.

Equity must participate in the adaptation premium. When a district improves through strategic repositioning and active stewardship, values rise. Under conventional structures, that premium accrues to whoever holds the deed. Adaptive equity, whether patient capital with longer carry, shared appreciation arrangements, or the Perpetual Purpose Trust structures we discussed in the last post, is designed to participate in that uplift and recycle it into continued stewardship. The flywheel only turns if equity captures what it helped create.

Public capital has a role that is neither subsidy nor charity. Government should act as risk-bearer of first resort, through first-loss positions, guarantee structures, or development finance that accepts non-standard returns, creating the conditions under which private capital can enter System B at the scale the problem requires. This is co-investment in genuine uncertainty, structured to share both risk and reward.

Blending these non-standard approaches into a System B-specific ‘adaptive capital stack’ is challenging. Investment in this asset class requires building new financial muscles. Those investors who can master it will have significant competitive advantage as cities lift out of doom loop spirals.

The four instruments outlined above constitute what we call Adaptive Finance: new valuation methods that see option value, new debt instruments that accommodate transition, new equity structures that participate in the adaptation premium, and public capital that de-risks the entry point without crowding out the market. Together, these can create a capital stack designed for System B on System B’s terms, rather than System A instruments applied to buildings that have already been left behind.

For the past five years, pundits across the country have framed Portland’s downtown as a cautionary tale, the poster child of the doom loop. We believe it can become a proving ground for a new kind of real estate finance. We’re ready for adaptation.

In the next installment, we’ll turn to the buildings themselves and the need for an adaptive design imperative.

Subscribe to Field Discovery to follow the series.

According to Cushman Wakefield’s 2025 Office Marketbeat: “Four-quarter rolling net absorption – a better measure of underlying demand since it smooths out quarterly volatility – exceeded 5.2 msf, its highest total since the first half of 2020. As has consistently been the case, higher-quality office space is outperforming the broader market.”